Who Says Brain Cancer is Uninvestable?

The Conventional Wisdom may need adjustment as better science emerges

Background

Over the past several decades, it has been challenging to attract meaningful investment for the development of new treatments for brain cancers. In particular, GBM or high grade gliomas (HGGs) are considered “radioactive” by many institutional and strategic investors owing to a dismal track record of clinical failures coupled with modest total addressable market size.

To be fair, GBM/HGG is one of the most challenging therapeutic areas in oncology development. One is hard pressed to find another cancer phenotype in the which the tumor microenvironment (TME) is as highly heterogeneous, invasive and immunosuppressed as one sees in GBM/HGG. Add to that an anatomical location in the brain and behind the blood brain barrier (BBB), and a very challenging situation arises.

The situation has been compounded by a research environment that has been out-of-touch with the forefront of modern molecular oncology and immuno-oncology. As a longtime Biotech entrepreneur and former Venture Partner at a large Tier 1 multi-strategy fund, the quality of the science that we have seen associated with Neuro-Oncology was substandard relative to other areas of Oncology. It is difficult to recommend a substantial Series A investment of $50-100 million when investigators or companies cannot elucidate a mechanism of action for a therapeutic candidate, and have not employed state-of-the-art molecular and cellular techniques in an effort to figure things out. Moreover, a clinician-led environment in which single agents lacking sound mechanistic rationale are thrown against the wall like therapeutic spaghetti is not a situation that raises the confidence of investors, or for that matter, patients.

A Path Forward

Given the extensive heterogeneity and immunosuppression in the human GBM/HGG TME, the most important lessons that we have learned are:

1. Single target monotherapies are not a winning strategy. The TME is too heterogeneous, and a result of atypical genetic/molecular flux (e.g. ecDNA), is too fluid to expect that a single target can be anything other than transiently useful.

2. In a combination strategy, it is essential that one element of the combination must induce immunological response. The highest frequency of clinical Objective Responses (ORs) that we see result from using a form of immunotherapy with a TME that has been converted to Hot (pro-inflammatory) instead of the baseline Cold (immunosuppressed) status. Surprisingly, one does not necessarily need a pharmacological intervention to flip the TME to Hot. Directed energy of modest power delivered by medical devices and tuned to particular resonant frequencies of key molecular nodes/processes can trigger a molecular cascade that results in a Hot TME. An added advantage is that such approaches are relatively non-invasive and circumvent the BBB.

3. The Phase 0/Window of Opportunity clinical trial framework is gaining traction. We do not know of a validated pre-clinical model of GBM/HGG that comes close to replicating the human clinical situation. As a result, brain cancer studies can produce remarkable results in animals, but utterly fail to translate into humans. This is particularly true of immunotherapy approaches. We have come to view pre-clinical models as useful for the assessment of safety margins and mechanistic rationale, but not much else. Employing Phase 0/Window of Opportunity clinical studies to quantitatively assess neuropharmacology and gain crucial evidence of mechanism translation is an idea whose time has come.

Brain Cancer is Investable

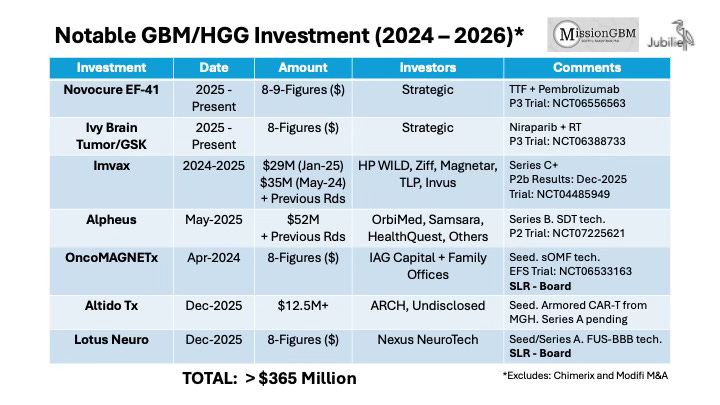

The nearby table summarizes selected investments in GBM/HGG companies and programs over the last 24 months. In order to preserve confidentiality, we have not listed the actual amounts invested nor the identities of some investors in the cases in which such information has not been otherwise publicly disclosed. Nonetheless, the aggregate amount of committed capital exceeds $350 million. If one includes other programs not featured in the table or resident within non-disclosing Biopharma companies, the figure rises to more than $400 million. Moreover, we are aware of three additional programs totaling another $200 million that are currently in fundraising or have raised funds but wish to remain in Stealth Mode. Of the seven programs in the table, five of them function via a mechanism that either directly or indirectly involves immunotherapy. In addition, four of the programs involve a novel medical device technology apart from radiotherapy.

Over the last four years, we have focused most of our time on identifying and working with investigators and companies that want to do things differently. An emphasis has been placed on those groups that are facile with modern molecular, cellular and immunological techniques and display a willingness to explore unconventional pathways in a rigorously scientific manner. We listen to hundreds of pitches each year; have provided uncompensated consulting advice to dozens of programs; have contributed Seed capital; and are delighted to socialize the best projects with our syndicate. We are not alone in this regard. Slowly, better science is emerging in Neuro-Oncology…and it is attracting meaningful investment.

We are not naïve. Nothing is more difficult than human clinical development, and it requires massive amounts of capital. Clinical setbacks are inevitable and several programs will fail to translate. Capital markets can be negatively impacted by both program-specific problems, macro trends such as geopolitical conflict and a rising cost of capital. But it is refreshing to see that a cadre of investors have stepped forward to nucleate significant investment in brain cancer based on improving science and a recognition of unmet clinical need.